Konstantin Poensgen

I am a PhD student in Economics at Harvard University. My research interests include public and development economics. I am a graduate student affiliate at the Harvard Center for International Development and the Minda de Gunzburg Center for European Studies.

Previously, I was a predoctoral fellow at the University of Zurich and a Junior Economist at the Organisation for Economic Co-operation and Development through the OECD Young Associates Programme (YAP). I hold a MSc in Econometrics and Mathematical Economics from the London School of Economics and a BSc in Economics from the University of Mannheim.

PhD and Predoc Application Resources

- Resources on PhD applications in economics

- Resources on predoc applications in economics (external link)

Working Papers

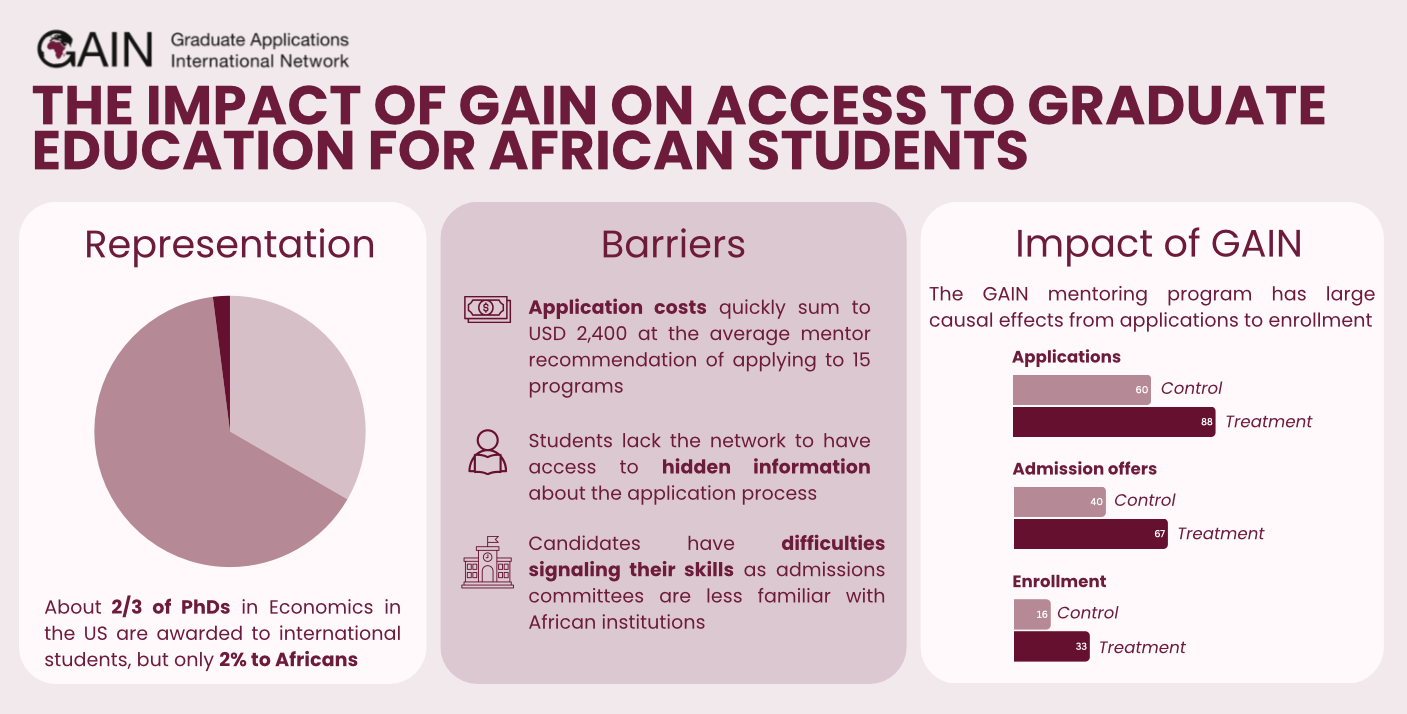

Applying to International Opportunity: Financial Assistance and Mentorship for Graduate School Applicants from Africa

with Samira Adhar and Frank Odhiambo (2026)

Summary Blog | RCT registration AEARCTR-0014352

Abstract

Students from lower-income countries face substantial barriers in accessing education abroad, shaping individual opportunity and global talent allocation. In a large sample of African prospective applicants, we document financial constraints, information gaps, and signaling frictions as first-order barriers in graduate school applications. Using a randomized controlled trial with high-achieving African candidates, we study whether application-stage financial assistance and mentorship relax these constraints. Overall, enrollment in Europe or North America nearly doubles from 16% in the control group. The program substantially reduces financial barriers to apply and increases applications on the level candidates are prepared for. PhD applications increase for candidates considered competitive for PhDs at baseline, who are then significantly more likely to obtain funded offers and enroll. Master's applications increase for those considered competitive at that level, but while they receive more admission offers, these are predominantly unfunded and there is no treatment effect on enrollment due to attendance costs. In terms of further mechanisms, the program does not strengthen the application profiles of candidates. Better mentor advice and advocacy positively correlate with enrollment, suggesting complementarities with financial support.

Tax Knowledge in Equilibrium: Evidence from an Education Program in Ghana

with Anders Jensen and Nikhil Kumar (2026)

RCT registration AEARCTR-0015079

Abstract

A property tax experiment in Ghana randomly provides tax education to property owners and officials. The intervention raises tax knowledge and generates spillovers to untreated households through conversations with more knowledgeable neighbors but has no ultimate impact on tax payments. Educated taxpayers and officials become more engaged in their interactions, but do not shift toward collaborative relationships. Taxpayers revise downward their beliefs about enforcement capacity and become more aware of legal ways to reduce their tax burden. These results highlight that tax knowledge spreads through social networks, and that its effects on tax outcomes are mediated by its ability to shape citizen–state interactions.

Statutory Incidence of Ad Valorem Taxes: Revisiting Classical Theory and Policy Implications

with Lukas Rodrian

Updated May 2026 | SSRN WP 5232926 (2025)

Materials: graphs / files

Abstract

This paper revisits the canonical result that statutory tax incidence is theoretically irrelevant for economic outcomes in competitive equilibrium. Shifting statutory incidence of ad valorem taxes toward the demand side reduces consumer prices, raises supplier prices, and increases quantity, whereas the effect on tax revenue is ambiguous. Changes in the tax base and effective tax rates explain these results. We derive new empirically tractable incidence formulas in response to statutory incidence shifts, which we quantify using simulations in the payroll tax context. We apply our framework to OECD payroll taxes, documenting that employer shares rise with total payroll taxes and offset nominal tax differences. These stylized facts further highlight the importance of accounting for statutory incidence in policy and empirical analyses. Finally, our incidence formulas provide a new methodology to point-identify elasticities and parameters like tax evasion, which we demonstrate using reduced-form estimates of price and quantity changes after a statutory incidence shift in Airbnb rental taxes.

Policy Papers

Global Landscape of Financing for Sustainable Development

OECD (2020), Global Outlook on Financing for Sustainable Development 2021: A New Way to Invest for People and Planet, OECD Publishing [Chapter 2]

OECD (2020), The impact of the coronavirus (COVID-19) crisis on development finance, OECD Policy Responses to Coronavirus (COVID-19) [with Thomas Rieger]

Health Sector Financing in Developing Economies

OECD (2021), Financing transition in the health sector: What can Development Assistance Committee members do?, OECD Development Policy Papers, No. 37 [with Jieun Kim and Martin Kessler]

OECD (2020), Strengthening health systems during a pandemic: The role of development finance, OECD Policy Responses to Coronavirus (COVID-19) [with Jieun Kim and Martin Kessler]

Financing Transitions across Development Stages

My work on development transition finance includes the OECD Transition Finance Toolkit. This toolkit allows analysts and decision-makers to conduct a transition finance diagnostic using a wealth of socio-economic and financial development indicators.

Cattaneo, O., C. Piemonte and K. Poensgen (2020), Transition finance country study of Chile: Better managing graduation from ODA eligibility, OECD Development Co-operation Working Papers, No. 70

Chiofalo, E., K. Poensgen and Y. Rockenfeller (2019), Transition finance country study of Lebanon: Global public goods and the response to adverse shocks, OECD Development Co-operation Working Papers, No. 61

Kim, J. and K. Poensgen (2019), Transition Finance Country Study Viet Nam: On the threshold of transition, OECD Development Co-operation Working Papers, No. 60

Kim, J., et al. (2018), Transition Finance Challenges for Commodity-based Least Developed Countries: The example of Zambia, OECD Development Co-operation Working Papers, No. 49

Morris, R., O. Cattaneo and K. Poensgen (2018), Cabo Verde Transition Finance Country Pilot, OECD Development Co-operation Working Papers, No. 46

OECD (2020), Transition finance ABC methodology: A user’s guide to transition finance diagnostics, OECD Development Policy Papers, No. 26 [with Abdoulaye Fabregas]

Piemonte, C., et al. (2019), Transition Finance: Introducing a new concept, OECD Development Co-operation Working Papers, No. 54